28 Exponential distribution

An exponential random variable \(X\) is defined only on the positive real line, i.e. \(X \in [0, \infty)\), and its distribution depends on a parameter \(\lambda > 0\) called rate.

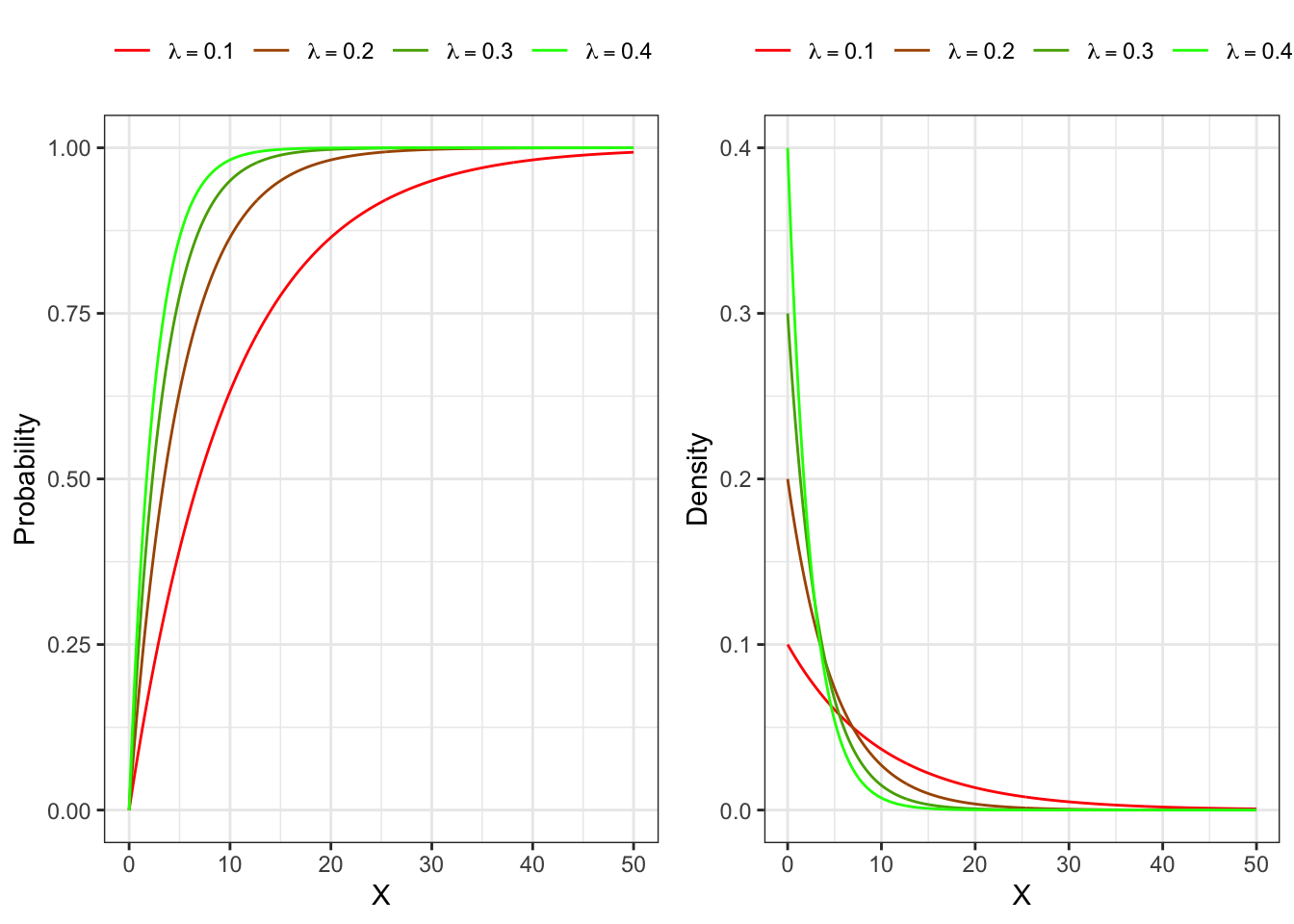

28.1 Distribution

The distribution function of an exponential random variable reads \[ F_X(x) = 1 - e^{-\lambda x} \text{,} \quad x \in [0, \infty) \text{.} \tag{28.1}\] Symmetrically, the survival function \(\bar{F}_X(x) = 1 - F_X(x)\) reads \[ \bar{F}_X(x) = e^{-\lambda x} \text{,} \quad x \in [0, \infty) \text{.} \] Taking the derivative with respect to \(x\) of Equation 28.1 gives the density function, i.e. \[ f_X(x) = \lambda e^{-\lambda x} \text{,} \quad x \in [0, \infty) \text{,} \]

28.2 Quantile

The quantile function of an exponential random variable is defined as \[ q_X(\alpha) = -\frac{1}{\lambda}\log(1-\alpha) \text{,} \quad \alpha \in [0, 1] \text{,} \]

Proof. The quantile function of a random variable is implicitly defined as the level of \(X = q_X(\alpha)\) such that the distribution function computed in \(q_X(\alpha)\) gives a probability equal to \(\alpha\). More precisely, one must solve for \(q_X(\alpha)\) such that: \[ \alpha = F_X(q_X(\alpha)) = 1 - e^{-\lambda q_X(\alpha)} \implies q_X(\alpha) = -\frac{1}{\lambda}\log(1-\alpha) \]