27 Bernoulli random variable

27.1 Distribution and density

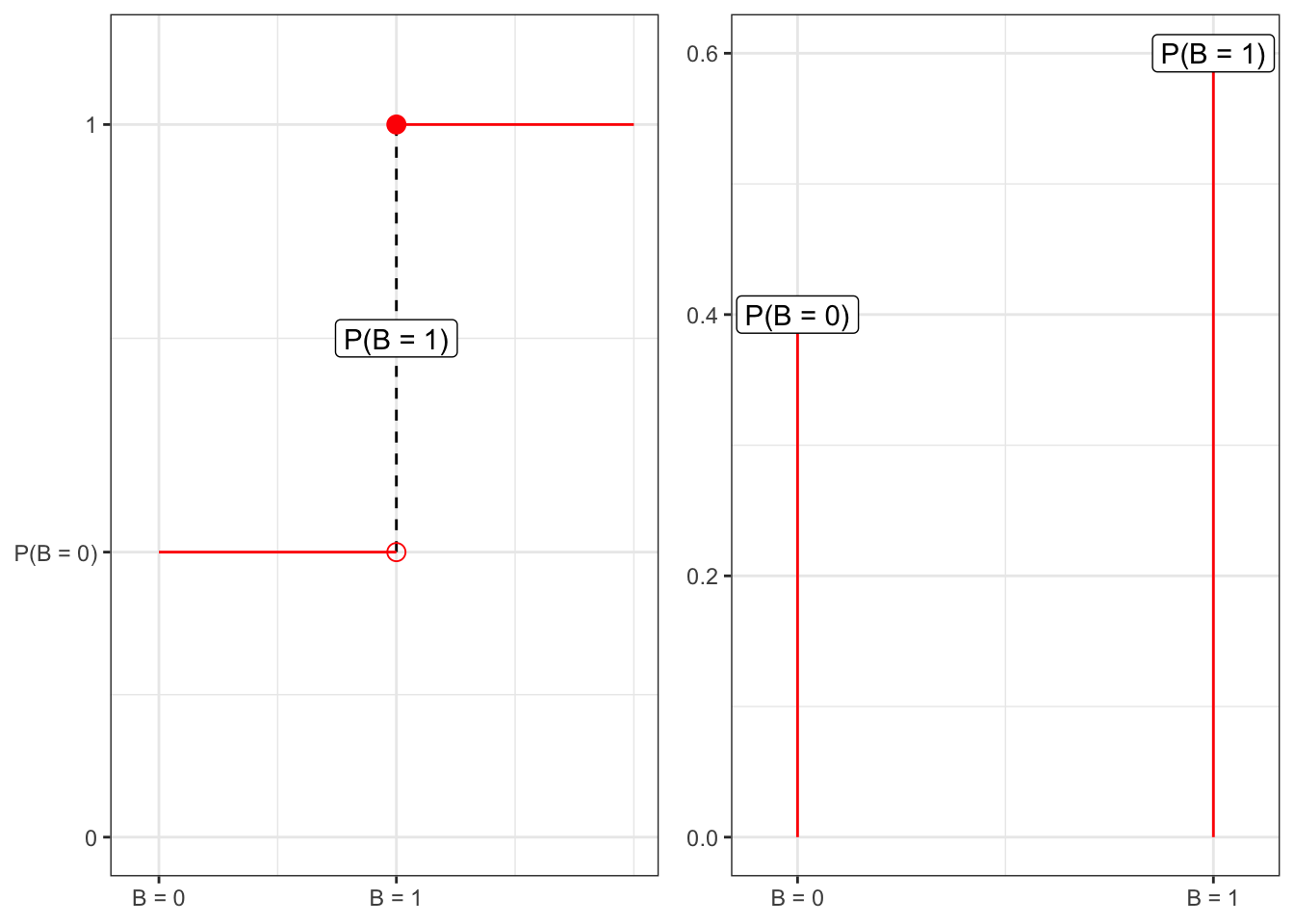

Definition 27.1 To construct the distribution function for a Bernoulli random variable, one can use the linear combination of two Heaviside functions (Equation 1.10), i.e. \[ F_B(x) = H(x) (1-p) + H(x-1) p \text{.} \tag{27.1}\] Given that the distribution function is specified in terms of Heaviside functions, it is possible to take the derivative with respect to \(x\) to obtain the density function, i.e. \[ f_B(x) = \delta(x) (1-p) + \delta(x-1) p \text{,} \tag{27.2}\] where \(\delta(x)\) is the Dirac function (Equation 1.11).

27.2 Characteristic function

Proposition 27.1 The characteristic function of a Bernoulli random variable reads explicitly: \[ \phi_B(t) = p e^{i t} + (1-p) \text{,} \tag{27.3}\] and similarly the moment generating function \[ \psi_{B}(t) = p e^{t} + (1-p) \text{.} \tag{27.4}\]

27.3 Moments

Proposition 27.2 The \(n\)-th moment of a Bernoulli random variable with probability \(p\) reads \[ \mathbb{E}\{B^n\} = \mathbb{P}(B = 1) = p \text{,} \] for all \(n \in \mathbb{N}\).